“If I have seen further than others it is because I have stood on the shoulders of giants” ( Isaac Newton)

Dear fellow business owners

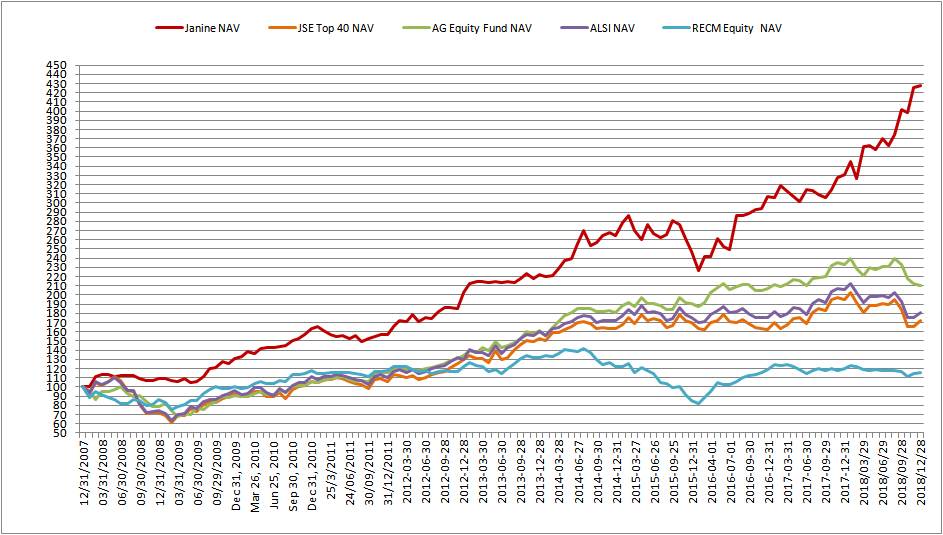

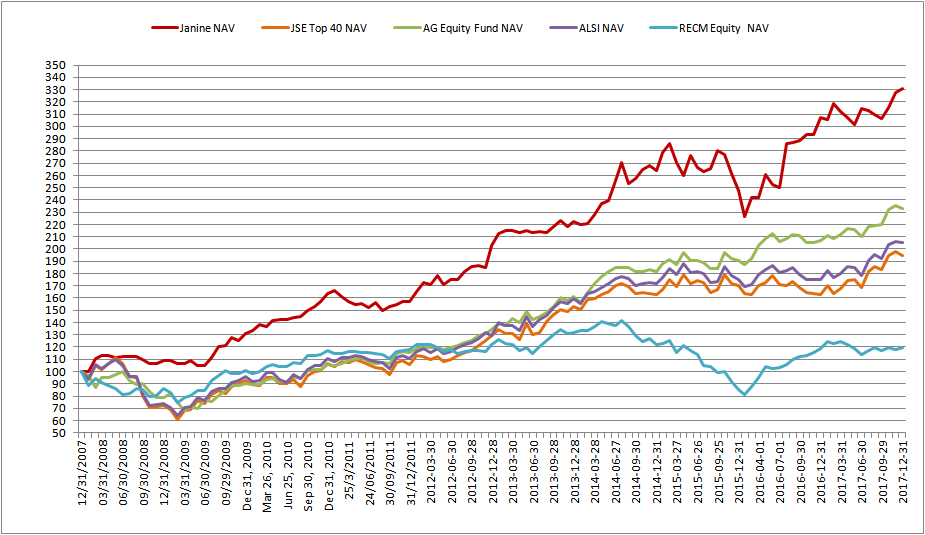

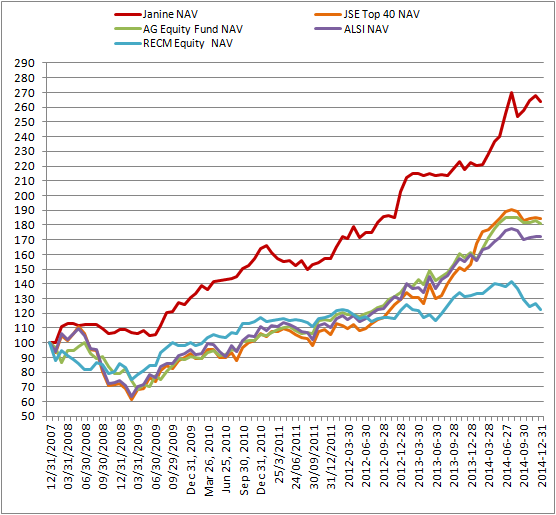

I’ve set myself a goal to learn as much as I can from successful investment-, as well as business managers as I could. It is a journey with no end destination and a life long dedication in order to be as successful in investing as I’ve set my goals to be.

In my quest to find honest managers, of money and businesses, I recently discovered Howard Marks. His memo’s to his clients over the years was just released recently on their website . His firm Oaktree Capital has an enviable record and he was also asked to write the foreword for one of the chapters in the newest edition of Security Analysis, by Graham and Dodd, the bible of Investment Analysis. For those interested, a very good interview with him can be read in the newest newsletter of Graham en Doddsville at the following link, http://www4.gsb.columbia.edu/null/download?&exclusive=filemgr.download&file_id=7212104 .

In my reading of his past memo’s, I came upon the one he wrote in 2004, Hey, Steward ! . Here he discusses the breaking down of fiduciary duties of the mutual fund industry and how “Amassing assets under management became the [mutual fund] industry’s primary goal, and how their focus shifted from stewardship to salesmanship.” (Emphasis added). Then lastly he focuses on those fiduciary duties of directors and professional managers of public companies. The whole memo is an excellent read but it is this second part that I quote hereunder which is especially relevant in these days.

Enjoy !!

What Else?

I want to make it clear that just as I do not universally indict mutual fund executives and directors, I don’t think stewardship problems exist only in the mutual fund industry. Most of the shortcomings disclosed in the corporate scandals of 2001-02 – in Enron, WorldCom, Adelphia, HealthSouth and Tyco – stemmed from the failure of executives to act on behalf of the shareholders who own the companies, and from the

failure of directors to police the executives.

The examples are endless: excessive compensation, unwarranted expenditures, phony accounting, and transactions intended only to deceive or obfuscate. In general, executives forgot that they run companies for their owners and instead tried to turn them into personal piggybanks. Or they decided to eschew honest reporting in order to hype results and thus their own economics. Directors of these companies haven’t been accused of wrongdoing, just underachieving. They were too complacent and obliging, and thus asleep at the switch. As Warren Buffett says, “sadly ‘boardroom atmosphere’ almost invariably sedates their fiduciary genes.”

The fundamental questions regarding corporate directors and executives are the same as those I proposed earlier regarding mutual funds: How much ends up in the pockets of the company and its owners, and how much in the pockets of the stewards? What means are used to accomplish this “wealth transfer”? How much is disclosed, and how clearly?

A number of thought-provoking examples were discussed in the Wall Street Journal of December 29, under the headline “Many Companies Report Transactions With Top Officers; ‘Related Party’ Deals Disclosed By 300 Large Corporations; Potential for Conflict.” The article discussed not the headline-grabbing misdeeds of the scandal era, but matters that are routine at America’s largest corporations. Often called “related-party transactions,” they represent deals through which directors or executives receive benefits beyond their standard compensation. Of course, there’s only one possible source for this enrichment: the companies and their shareholders. The Journal and I draw no conclusion about whether these things are proper. But they certainly can serve as fodder for discussing the performance of stewards. Here are a few examples:

A company employs or has business ties with 17 relatives of senior officials.

An executive is reimbursed for making business trips on his airplane.

A company buys “financial advisory services” from a director’s company.

Directors receive hundreds of thousands of dollars in consulting fees, above and beyond their directors’ fees. The fees reward the director/consultants for supplying “general information” or “maintaining and enhancing the company’s strategic alignment.” In the latter case, the recipient happens to be the company’s second-biggest shareholder.

A lawyer serves on a corporate board, and the company gives legal work to his firm.

The son-in-law of a former board chairman runs a real estate joint venture involving the company, to which the company guarantees a minimum level of profitability.

A company sells an amusement park to its controlling shareholder, with the buyer paying half the purchase price in the form of passes to the amusement park he just bought.

The Journal put it succinctly. “All these deals present the risk of conflicts between a company official’s two roles: representative of the shareholder and individual seeking to get the best deal for himself.” They raise significant questions:

Are these deals negotiated at arm’s length? Are the terms the best the company can get?

Who negotiates on behalf of the shareholders? How vehemently?

Where a deal is proposed by a shareholder or shareholder/director with a dominant ownership position, who stands up for the minority shareholders?

How can we be sure director A won’t simply vote for director B’s excessive deal in exchange for director B returning the favor?

As I mentioned above, there has been no allegation – even in Enron, Tyco and Adelphia – of actual director impropriety. Rather, the questions surround the energy put into governance.

After working together for many years, directors develop congenial relationships with each other and with the executives. How strongly will they then fight to resist questionable transactions between the company and their colleagues?

Directors’ fees can run into the hundreds of thousands, perhaps with stock options and perks in addition. Will a director risk this package to fight for some faceless shareholders?

In short, can a director who serves at the pleasure of the chairman police the chairman and his other handpicked directors and executives? How can directors be guaranteed the independence that shareholders need them to have?

The industrial economy achieved great strides because of a number of advances, one of which was the separation of management from ownership (and the accompanying development of a class of professional managers). The caveat, of course, is that managers and directors must serve diligently as stewards, protecting the interests of the firm’s absentee owners. The system only works if the stewards – entrusted with responsibility on behalf of others – are up to the task.

The Bottom Line

As you prepare your estate plan, you count on fiduciaries – lawyers, accountants, executors and trustees – to ensure that your assets will be disposed of as you intend. Would you want one of those fiduciaries to buy assets directly from your estate? Rent office space to your estate? Employ his relatives to serve your estate, for additional fees? Enter into a joint venture with the company you left behind? You’d expect the stewards of your estate to be “purer than Caesar’s wife.” Even with motivations that are entirely honorable, it would be impossible for your fiduciaries to simultaneously represent themselves and your heirs on opposite sides of a transaction and still maintain both the fact and the appearance of fairness. Thus they must content themselves with the compensation they’ve been assigned by you or by law. They must resist the temptation to do business with your estate in a way that could benefit them further . . . and to possibly move a little from your heirs’ pockets to their own. We must expect no less from the stewards that we and our companies do business with every day.

In my memos I try to resist citing Oaktree as the paragon of virtue. But when we founded our company, we established an acid test that we routinely rely on to keep us on the right track. It was stated in our original brochure in 1995, and it has served us well ever since.

It is our fundamental operating principle that if all of our practices were to become known, there must be no one with grounds for complaint.

To put it more simply, we assume everything we do will show up on “page one” some day – that nothing will remain a secret. Will there be a negative reaction? Will anyone object?

It’s a simple test, but it seems every day that the newspapers describe someone whose actions could only have been premised on the assumption that no one – not media, shareholders, clients, auditors or regulators – would learn the truth.

Will directors approve of executives’ actions? Will shareholders feel that directors did their job correctly? Will clients conclude that fiduciaries have put responsibility to them ahead of their own interests? We think the standards for stewards’ behavior are pretty clear cut, which means making these assessments shouldn’t be that hard.

March 16, 2004

Howard Marks